Money and Credit Notes

Introduction

Money is used to make transactions like buying and selling goods and services. money acts as an intermediate in the exchange process, it is called a medium of exchange.

Why is money used for transactions?

A person holding money can easily exchange it for any commodity or service that he or she might want.

Shoe manufacturer case

He wants to sell shoes in the market and buy wheat. The shoe manufacturer will first exchange shoes that he has produced for money, and then exchange the money for wheat.

Imagine how much more difficult it would be if the shoe manufacturer had to directly exchange shoes for wheat without the use of money. He would have to look for a wheat-growing farmer who not only wants to sell wheat but also wants to buy the shoes in exchange.

That is, both parties have to agree to sell and buy each other’s commodities. This is known as

a double coincidence of wants. What a person desires to sell is exactly what the other wishes to buy. This system is known as the barter system.

Barter System Definition

The barter system is a method of exchanging goods and services without using money. In a barter system, people trade goods and services directly with each other, without using money. Double coincidence of wants is an essential feature of the barter system.

Currency

Modern physical forms of money are paper notes and coins.

Modern currency is not made of precious metals like gold, silver, and copper. Modern currency is found in paper notes and coins. A valid currency is only authorized by the government of the country.

In India, the Reserve Bank of India issues currency notes on behalf of the central government. As per Indian law, no other individual or organization is allowed to issue currency.

The rupee is widely accepted as a medium of exchange. The law legalizes that no individual or organization in India can legally refuse a payment made in rupees.

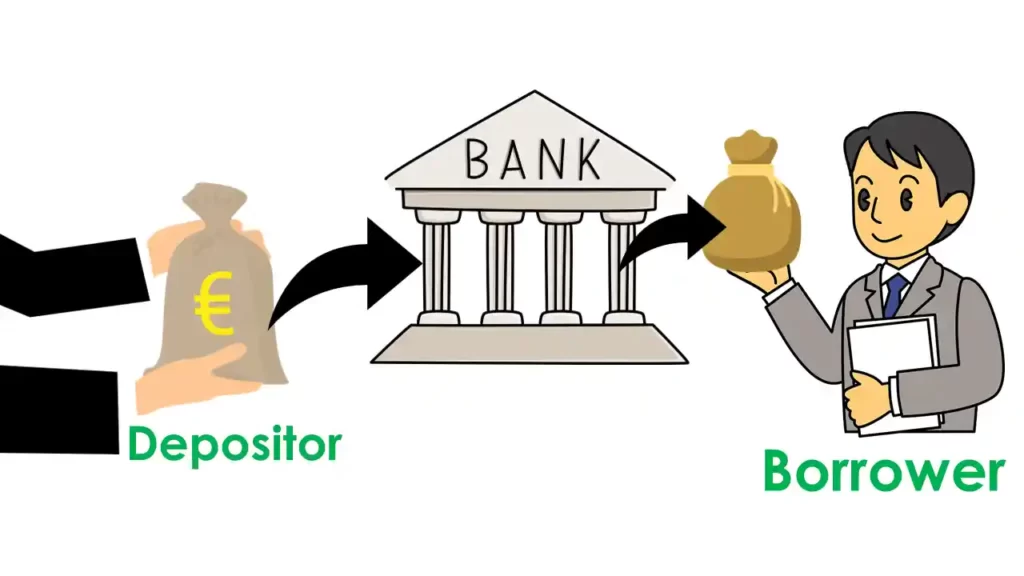

Deposits with Banks

Excess money except for day-to-day expenses we deposit it with the bank by opening a bank account.

Different types of Banks accounts are offered by the banks to their customers.

- Savings Account (for individuals who deposit and withdraw cash frequently)

- Recurring Deposit Account (a fixed amount deposit monthly for a particular period.)

- Current Deposit Account (opened by businessman for business transactions)

- Fixed Deposit Account (also known as term deposit, offered higher interest return on investment)

Why do we deposit our money into the bank?

Interest – Banks provide interest on deposits. It means you can earn more from the money that you have deposited with the bank.

Safety and Security – By depositing your money in a bank, it is protected from theft, loss, or damage.

Other benefits – Banks offer convenient access to money through ATMs, Online Banking, and Mobile Apps.

Depositing money in a bank account provides individuals with a secure and convenient way to manage their money, while also providing opportunities to earn interest and build financial stability.

What is a cheque?

A cheque is a paper instructing the bank to pay a specific amount from the person’s account to the person in whose name the cheque has been issued.

The facility of cheques against demand deposits makes it possible to directly settle payments without the use of cash. Since demand deposits are accepted widely as a means of payment, along with the currency.

What do the banks do with the deposits which they accept from the public?

- There is an interesting mechanism working here.

- Banks use the major portion of the deposits to extend loans.

- There is a huge demand for loans for various economic activities.

- Banks in India these days hold about 15 percent of their deposits as cash. This is kept as a provision to pay the depositors who might come to withdraw money from the bank on any given day.

- In this way, banks mediate between those who have surplus funds (the depositors) and those who require these funds (the borrowers). Banks charge a higher interest rate on loans than what they offer on deposits.

What is credit?

- Credit (loan) refers to an agreement in which the lender supplies the borrower with money, goods, or services in return for the promise of future payment.

- Credit is an important part of the economy, as it allows individuals and businesses to access funds and invest in opportunities that they may not be able to afford with cash on hand.

- Credit can come in many forms, including loans, credit cards, lines of credit, and mortgages.

What are the terms of credit?

The terms of credit vary from one credit arrangement to another. They may be depending on the nature of the lender and the borrower.

Every loan agreement specifies an interest rate that the borrower must pay to the lender along with the repayment of the principal. In addition, lenders may demand collateral (security) against loans.

What is a Collateral?

Collateral is an asset that the borrower owns (such as land, building, vehicle, livestock, and deposits with banks) and uses this as a guarantee to a lender until the loan is repaid.

Various sources of obtaining credit

- Some people would borrow money from moneylenders at a certain interest rate.

- Some people would take bank loans at the interest rate.

- Some people take from the landowner at the interest rate.

- The other major source of cheap credit from cooperative societies.

The various types of loans can be divided into two types.

- Formal sector loans

- Informal sector loans

1. formal sector loans

- The Reserve Bank of India supervises the functioning of formal sources of loans.

- The RBI monitors the banks in actually maintaining cash balances.

- The RBI sees that the banks give loans not just to profit-making businesses and traders but also to small cultivators, small-scale industries, small borrowers, etc.

- while formal sector loans need to expand, it is also necessary that everyone receives these loans.

2. informal sector loans

- No organization supervises the credit activities of lenders in the informal sector.

- They can lend at whatever interest rate they choose.

- There is no one to stop them from using unfair means to get their money back.

- If many people could then borrow cheaply for a variety of needs.

- They could grow crops, do business, set up small-scale industries, etc.

- They could set up new industries or trade in goods.

- Cheap and affordable credit is necessary for the country’s development.

Thus, banks and cooperatives must increase their lending, particularly in rural areas, so that the dependence on informal sources of credit reduces.

Why do poor householders depend upon informal?

- Banks are not present everywhere in rural India. Even when they are present, getting a loan from a bank is much more difficult than taking a loan from informal sources.

- Bank loans require proper documents and collateral.

- The absence of collateral is one of the major reasons which prevents the poor from getting bank loans.

- Informal lenders such as moneylenders, on the other hand, know the borrowers personally and hence are often willing to give a loan without collateral.

- If necessary, the borrowers can approach the moneylenders even without repaying their earlier loans.

- However, the moneylenders charge very high rates of interest, keep no records of the transactions and harass poor borrowers.

What are Self Help Groups (SHGs)?

- The idea is to organize the rural poor, in particular women, into small Self-Help Groups (SHGs) and pool (collect) their savings.

- A typical SHG has 15-20 members, usually belonging to one neighbourhoods, who meet and save regularly.

- Saving per member varies from Rs 25 to Rs 100 or more, depending on the ability of the people to save.

- Members can take small loans from the group itself to meet their needs.

- The group charges interest on these loans but this is still less than what the moneylender charges.

- After a year or two, if the group is regular in savings, it becomes eligible for availing loan from the bank.

- Thus, the SHGs help borrowers overcome the problem of lack of collateral. They can get timely loans for a variety of purposes and at a reasonable interest rate.

Related Links

- CBSE 10 Polity Chapter 5 Outcomes of Democracy Questions and Answers

- CBSE 10 Polity Chapter 5 Outcomes of Democracy Notes

- CBSE 10 Chapter 4 Political Parties Questions and Answers

- CBSE 10 Polity Chapter 4 Political Parties Notes

- CBSE 10 Polity Gender, Religion and Caste Questions and Answers

- CBSE 10 Polity Chapter 3 Gender Religion and Caste Notes

- CBSE 10 History Chapter 5 Print Culture and the Modern World Questions and Answers

- CBSE 10 History Chapter 5 Print Culture and the Modern World Notes

- CBSE 10 History Chapter 4 The Age of Industrialisation Questions and Answers

- CBSE 10 History Chapter 4 The Age of Industrialisation Notes

- The making of the global world Questions and Answers

- The Making of Global World Notes

- CBSE 10 Economics Chapter 5 Consumer Rights Questions and Answers

- CBSE 10 Economics Chapter 5 Consumer Rights

- CBSE Class 10 economics chapter 3 Money and Credit Questions and Answers

- CBSE class 10 Economics chapter 3 Money and Credit Notes

- CBSE 10 Geography Lifeline of National Economy Notes

- CBSC 10 Lifeline of National Economy Questions and Answers

- CBSE 10 Geography chapter 3 Water Resource Questions and Answers

- CBSE 10 Geography Chapter 2 Forest and Wildlife Resources Questions and Answers

- Greenhouse gases and its Effects

- Motion in Physics – Definition, Laws, Types of Motion

- Sound and its related terms

- Differences between Unicellular and Multicellular Organism

- Differences between Plant cell and animal cell

- Cell Structure and Functions list

- Elements and their Symbols with atomic numbers

- First 118 elements of the periodic table with their symbols and typical valences

- List of Important Abbreviations for various competitive exam

- Human Body Facts

- Branches of Biology

- Democracy Government

- 11 Famous Slogans of Indian Freedom Fighters

- Fundamental Rights

- Writs of the Indian Constitution

- Computer Networking notes

- Class 10 Rabi, Kharif and Zaid Crops notes

- List of Computer Abbreviation

- List of people considered father or Mother of a field in India

- Red and Yellow Soil